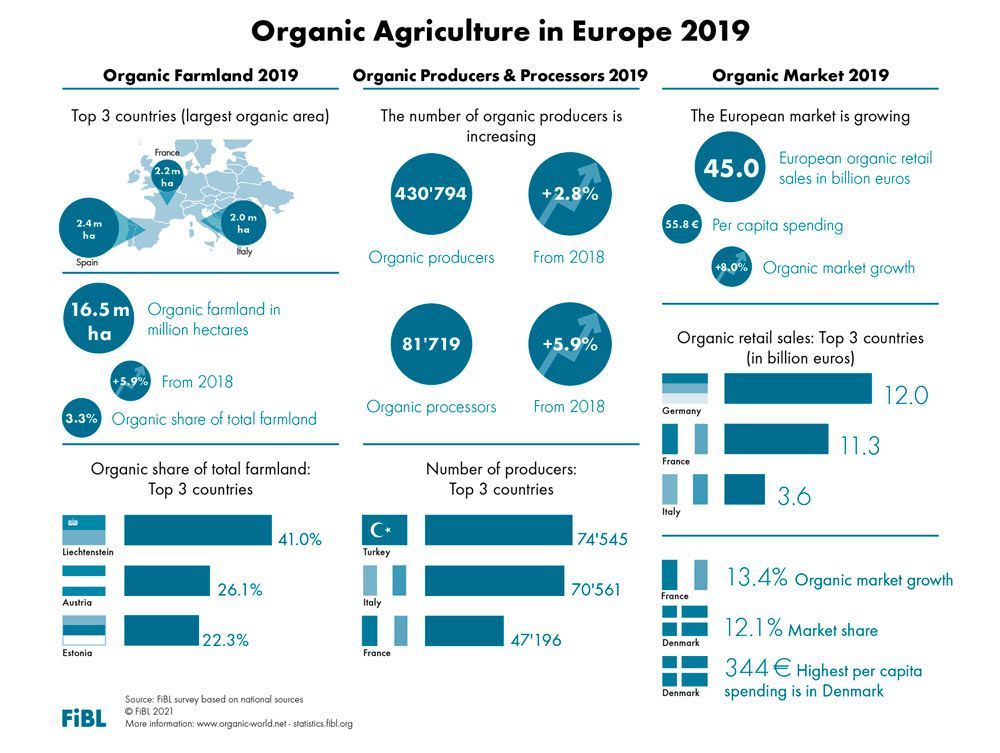

The European organic market continues to grow. In 2019, it increased by another 8 percent and reached €45.0 billion. Some markets enjoyed double-digit growth rates.

Source: FiBL

At this year’s digital edition of BIOFACH, the world’s leading trade fair for organic food, the Research Institute of Organic Agriculture FiBL, the Agricultural Market Information Company AMI and partners are presenting the data on the European organic sector (BIOFACH eSPECIAL, 17 February 2021, from 5 to 6 pm, Livestream 5).

European organic market experienced a substantial growth

In Europe, 16.5 million hectares of farmland were organic in 2019 (European Union: 14.6 million hectares). With almost 2.4 million hectares, Spain continues to be the country with the largest organic area in Europe, followed by France (2.2 million hectares), and Italy (2.0 million hectares).

Source: FiBL

Organic farmland increased by almost one million hectares

The organic farmland increased by over 0.9 million hectares in Europe and by over 0.8 million hectares in the European Union, representing an increase of 5.9% each. Growth was slower than in 2018 but higher than in the first years of the past decade. France reported almost 206’000 hectares more than in 2018, Ukraine almost 159’000 hectares more, and Spain over 108’000 hectares more.

The organic farmland increased by over 0.9 million hectares in Europe

Liechtenstein is the country with the highest organic share of the total farmland in the world

In 2019, organic farmland in Europe constituted 3.3% of the total agricultural land and 8.1% in the European Union. In Europe (and globally), Liechtenstein had the highest organic share of all farmland (41.0%) followed by Austria, the country in the European Union with the highest organic share (26.1%). Twelve European countries reported that at least 10% of their farmland is organic.

Organic producers on the rise

There were almost 430.000 organic producers in Europe and almost 343.000 in the European Union. The largest numbers were in Turkey (almost 74.545) and Italy (70.561). The number of producers grew by 2.8% in Europe and by 5.0% in the European Union.

Continued growth of processors and importers

There were almost 82.000 processors in Europe and over 78.000 in the European Union. Over 6.500 importers were counted in Europe and almost 5.800 in the European Union. The country with the largest number of processors was Italy (nearly 22.000), while Germany had the most importers (more than 1.800).

Retail sales reach €45.0 billion

Retail sales in Europe were valued at €45.0 billion (€41.4 billion in the European Union). The largest market was Germany (€12.0 billion). The European Union represents the second largest single market for organic products in the world after the United States (€44.7 billion).

The European Union represents the second largest single market for organic products in the world

Steady growth of retail sales in 2019

The European market recorded a growth rate of 8.0%. Among the key markets, the highest growth was observed in France (13.4%). In the decade 2010-2019, the European and European Union markets’ value has more than doubled.

European consumers spend more on organic food

In Europe, consumers spent 56€ on organic food per person annually (European Union: 84€). Per capita, consumer spending on organic food has doubled in the last decade. In 2019, Danish and Swiss consumers spent the most money on organic food (€344 and €338 per capita, respectively).

Denmark has the highest organic market share in the world

Globally, European countries account for the highest shares of organic food sales as a percentage of their respective food markets. Denmark has the highest organic food sales share worldwide, with 12.1%in 2019, followed by Switzerland with a share of 10.4% and Austria with 9.3%.

Quotes

According to Helga Willer, responsible for data collection at FiBL, the numbers for 2019 show a promising growth of the organic area and market. “However, the organic area will have to continue to grow in the coming years in order to reach the European Commission’s goal of 25% organically farmed land by 2030”.

Eduardo Cuoco, Director at IFOAM Organics Europe, continued: “This data shows the European organic market’s potential to reach the objective of 25% organic land by 2030 put forward in the EU Biodiversity and Farm to Fork strategies. To reach this target the organic sector needs political support at all levels. This includes a good regulatory framework, adequate support under the CAP – with clear support for organic in the national strategic action plans – and a powerful European Organic Action Plan with concrete actions supporting conversion, market development and capacity building of the European organic sector. We will work closely with all the stakeholders to develop tools to measure and support organic growth”.

“The numbers for 2019 show a promising growth of the organic area and market”

Diana Schaack, a market analyst at AMI, adds: “We are already looking forward to the consolidated market data for 2020. Last year the organic market in many countries exhibited accelerated growth due to the pandemic. If this trend sustains, production and processing have to keep pace. The Farm to Fork strategy of the European Union can support this development with respective measures”

FiBL and AMI conducted the survey on organic farming in Europe. The FiBL data collection was carried out in the framework of the global survey on organic farming supported by the Swiss State Secretariat for Economic Affairs (SECO), the International Trade Centre (ITC), the Coop Sustainability Fund, NürnbergMesse and IFOAM – Organics International.

Over 72.3 million hectares of farmland are organic & market reached 106 billion euros

- Further information available at www.fibl.org

Subscribe to Bio Eco Actual Newsletter and be up to date with the latest news from the Organic Sector

Bio Eco Actual, International Organic Newspaper

Read Bio Eco Actual